ISM Manufacturing Ouput

The Institute for Supply Management has reported that new orders continue to grow strongly, but supply chain issues appear to be holding back production. Consequently, we are seeing record high order backlogs. This in itself presents an opportunity for more growth in ouput because of the high demand. It also presents and opportunity for job creation. Lets take a closer look at the numbers. US manufacturing output increased 0.9% in May versus the consensus of 0.8% but the April number was revised down significantly to an output growth of 0.1% versus the 0.5% rate initially reported. This leaves manufacturing output down by 0.7% on the pre-pandemic peak, having fallen 19.8% from the peak in January to the trough in April last year. The future is looking brighter with a full recovery in manufacturing output expected in the next few months. However, given the high demand and supply chain issues, there is a real risk of prices rising significantly if this situation persists. Retail Sales US retail sales dipped in May but they remain very strong as the economy re-opens and consumers want to spend their money and enjoy some retail therapy! US retail sales were down 1.3% month-on-month in May, but some of this can be offset by significant upward revisions. April’s month on month figure of 0% has been revised up to 0.9% growth. The details show auto sales were down 3.7% month on month, which may well be caused by a slow down in production due to supply chain issues. Eating and drinking continued to make a recovery (+1.8%) which is the third consecutive monthly gain. Coming after the significant upward revisions in the April figure and the surge of 11.3% in March driven by stimulus, the dip in May's retail sales aren't too shabby. Consumer Finances Last week's Federal Reserve flow of funds data showed households have seen their wealth surge $20tn since the end of 2019 with $3tn of that increase in liquid cash, checking and time savings deposits. Consumer finances are in good shape and with this kind of financial firepower, there is a lot of support for consumer spending that could go on for many months yet. PPI & Pipeline Price Pressures We have also had the producer price inflation report which showed a pick-up in inflation with month on month price rises hitting 0.8% versus the 0.5% consensus. Excluding food and energy, the numbers came in at 0.7% versus 0.5% forecast. Food showed the second consecutive 2%+ month on month reading while transportation and warehousing rose 1.9% month on month. Other components also posted sizeable gains, so this tells us that we've got some pipeline pricing pressure. Conclusion The ISM report showed that the order books continue to grow strongly, but production is struggling to keep pace. The the backlog of orders has risen to new all-time highs while at the same time customer inventories are at record lows. So what does this tell us? Well, it certainly suggests that pipeline price pressures will continue to build, and this could lead to consumer price inflation staying higher for longer.

0 Comments

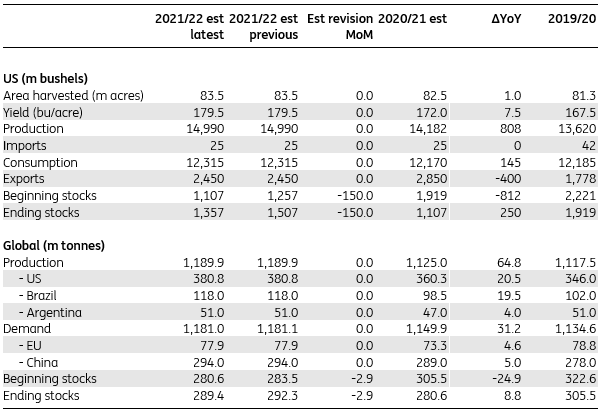

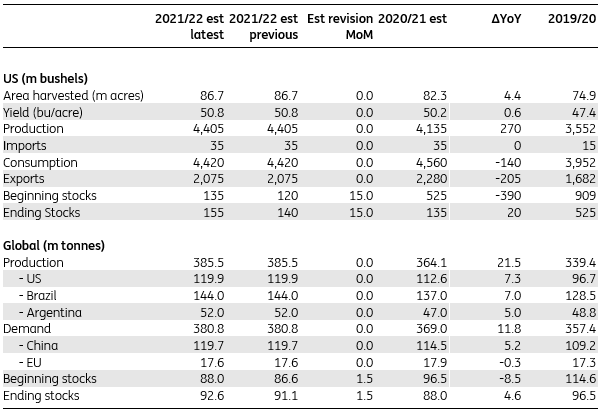

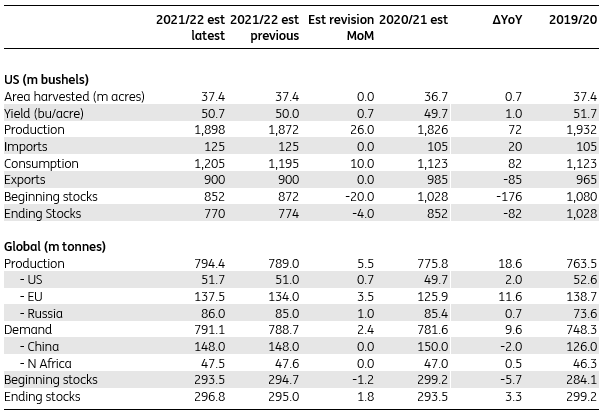

Corn The June WASDE report from the USDA was moderately supportive of corn prices, with changes to the US and global 2020/21 balance sheets leading to a tightening of supply. In the US, both domestic demand and export estimates were increased for the 2020/21 marketing year by a combined 150m bushels. Consequently, US ending stocks decreased to 1.1 billion bushels, which ws below expectations of about 1.2 billion bushels. For the 2021/22 season, there were no changes to the US corn balance. With regards to the global corn balance, the Brazilian corm crop had the largest change for the 2020/21 season. The drought conditions in the region has impacted the safrinha corn crop. The USDA revised the Brazilian production down to 98 million tonnes from 102 million tonnes, which still leaves output higher than expected. For 2021/22, global corn stocks are expected to grow year on year which means there is a probabaility that prices could weaken from current levels as the new corn crop becomes availble, but only if the weather through the summer months is favorable. So weather is the key factor to watch over the coming months. Another key factor is on the demand side and this is the Chinese imports through 2021/22 and wether we'll continue to see the level of demand that we did in 2020/21. The USDA is forecasting that China imports will total 26 million tonnes which is unchanged from eh current season's estimate. Corn Supply/Demand Balance  Source: USDA Soybeans The WASDE numbers were not as supportive for soybeans as they were for corn. The USDA revised their US domestic demand estimate by 15 million bushels for the 2020/21 marketing year, and consequentl, ending stocks are coming in at 135 million bushels which was higher then expectations of about 120 million bushels. With regard to the global soybean balance for 2020/21, the market is expecting to see ending stocks edge higher, with an estimate of 88 million tonnes which is anincrease over the previous estimate of 86.55 million tonnes and higher then expectations of about 87.4 million tonnes. The reason for these higher numbers is a softening of demand in the US and an increase in Brazilian production which was revised higher to 137 million tonnes from 136 million tonnes. The 2021/22 global balance sheet saw marginal changes to demand & supply, with higher ending stocks driven by expectations of a larger carryover of inventories from the current marketing year. As a result, global ending stocks for 2021/22 are forecast to increase to 92.55 million tonees with increased output from Brazil, the US and Argentina. This suggests a higher probability of soybean prices trending lower in the next marketing year, assumming that we don't any supply shocks to change the suplly and demand picture. Soybean Supply/Demand Balance  Source: USDA Wheat The WASDE reports hsowed the US wheat balance was largely unchanged for 2020/21, however, the USDA did revise the exports higher by 20 million bushels. This leaves ending stocks at 852 million bushels, which ws lower than expectations of about 870 million bushels. Consequently, beginning stocks for 2021/22 are a bit lower but this is offset by expectations of higher output in 2021/22. Ending stocks for 2021/22 are estimated at 770m bushels compared to market expectations of more than 780m bushels. With regard to the global balance, the USDA increased its supply estimates for 2021/22 on higher production from Europe, as recent rains were seen beneficial for the current crop. They also revised global production estimates higher. by 5.5 million tonnes witht he majority of this coming from Europe. Global production is now projected to increase 2.4% year on year to a record high of 794.4 million tonnes. Global demand estimates were also revised higher by around 3 million tonnes, which was mostly driven by Europe. Consequently, 2021/22 global ending stocks estimates were increased by around 1.8 million tonnes to 296.8 million tonnes, which was above market expectations of 294 million tonnes. Wheat Supply/Demand Balance  Source: USDA

This follows on from repeated warnings coming out of China from officals talking about high commodity prices after surging producer inflation strengthened China’s resolve to keep commodity prices in check. On Wednesday, China’s state planner renewed its pledge to step up monitoring of commodity prices and strengthen supervision of spot and futures markets, as domestic producer inflation hit its highest in more than 12 years. Indeed speculation continues about the potential for the China State Reserve Bureau (SRB) to release stock. At this point, they are essentially trying to talk the market down. This strategy could be working as some investors are becoming cautious and with unconfirmed talk of the SRB releasing copper, aluminium, and zinc stocks at the end of each month and we could see a steeper correction in the copper market over the coming weeks. Indeed, on the Thursday this week, the 3-month copper on the London Metal Exchange fell 0.6% to $9,920 a tonne early in the morning, while the most-traded July copper contract on the Shanghai Futures Exchange dipped 0.5% to 71,290 yuan ($11,167.15) a tonne. But copper prices have had a good run this surging by 28% on the LME and 21% on ShFE. Last month, both contracts hit record highs and looking very overbought on the charts. Therefore, a correction is quite likely at these levels and talk from China about price controls and rumours of releasing stock from the SRB will serve as a catalyst for the correction and we could see significant long liquidation. Inflation Narrative In addition, there is the narrative around US inflation and the market is awaiting the latest figures due out later on Thursday for clues the Fed's position on tapering. If there are any signals of tapering or even thinking about talking about tapering, then this could dampen demand for copper and metals in general. Developments in Peru The markets have also been focused on the Peruvian election results. If Castillo wins, this could add to the risk premium for long term copper mine supply. This is a long term narrative that mine investments may fall short of the expected surge in demand. Chinese Imports The customs dat on Monday showed that China’s copper imports fell 8% in May from the previous month, as record-high prices dampened demand from the world's largest importer and consumer of copper. Imports of unwrought copper and copper products came in at 445,725 tonnes in May. That was down from 484,890 tonnes in April for a second straight month-on-month drop but up from 436,030 tonnes in May 2020. Growth in China’s manufacturing sector, a key copper consuming sector, slowed slightly in May as raw materials costs rose at their fastest pace in over a decade. If we look at the Yangshan copper premium SMM-CUYP-CN, paid on top of London prices for delivery of physical copper into China, we see that it is at its lowest since 2016 at $28 a tonne. This just confirms the lower buying interst in China at this time. The record high copper prices hare causing some buyers in China to sit on the sidelines and manufacturers are reportedly trimming down operations. The increasing gap between Chinese PPI and CPI implies to some degree that many manufacturers stuck in the middle are absorbing the higher costs and this will dampen any appetite for stockpiling. By the end of May, the copper inventories in Shanghai bonded warehouses SMM-CUR-BON increased to 415,500 tonnes, which is the most the most since July 2019. Continued high prices are are likely to have an impact on future imports, however, even with the monthly declines, overall import levels are still relatively high. In Summary The market is getting cautious about China retreating in its copper purchases, but the recent weakness in prices has been seen across the industrial metals complex. Much of the market gyrations we have seen in recent markets closely track the broader macro market activities. There have been rising speculations on Fed tapering, and any signalling of the earlier tapering than expected will cauase the US dollar to rally, which will also have an impact on copper prices and commodities in general causing more downside pressure.

New orders confirm this as they increased to 67 from 64.3 and backlog orders were at all-time highs. This tells us that the US manufacturing sector continues to perform very strongly, but at the same time, supply chain issues are casuing a few problems for output and the knock on effect of this is increasing prices. We are also seeing delivery times increase to their highest since 1974 and no doubt impacted by shortages in the auto industry and challenges in recruiting workers.

Finding Workers The employment figures show there are challenges in finding workers. Home schooling has forced parents to say at home and indeed some people are in no rush to go back to work given the pandemic. The uprated unployment benefits are also not creating an incentive to return to work when taking into account childcare costs etc. Its unlikely that these factors will ease off any time soon and may impact the labour figures for some time to come. Struggling to Keep up with Demand Consumer demand is high following the lifting of COVID-19 restrictions and people want to spend some money. Inventories are at an all time low and those supply chain constraints are causing delays in replenishing inventory. Throw these into the melting pot and you've got a recipe for inflation. With high demand, constrained supply and increasing input prices, it's not dfficult to see inflation heading northward for some time to come and potentially more persistent than the Fed expects.

Annualised GDP growth in Q1 came in at 5.6%, whicih was was below the expectation of 6.3% growth. But we can't too disappointed by this miss to the downside because the Candian economy recovery is on the right track. Tle labour market is strong, fiscal policy is supportive, commody prices are rising and the vaccination program is going well.

A Good Mix of Growth The Canadian GDP shows growth in numerous areas. Consumer spending rose an an annualised rate of 3.4%, investment was up 17%, government was up 6.2% and net trade made a positive contribution. However, inventories subtracted 1.4% from the headline growth. This leaves GDP output 1.5 percentage points below the pre-pandemic peak and in the current quarter, there is a strong possibility of output being the same as or better than pre-pandemic lavels. Overall, its a good mix of growth. How Does Canada Compare with the US? The vaccination program has been firing on all cylinders and is currently getting turbo boost as it overtakes the US in terms of the proportion of the population haveing recieved at least one vaccination dose. In addition, the labour market is also bouncing back more strongly than in the US with employment just 2.4 percentage points below its pre-pandemic peak. In contrast, US employment is 5.4 percentage points below its pre-pandemic peak. Inflationary Pressures? Helping this along is the ongoing stimulus, and increasing commodity prices but is this causing inflation to run hot? Inflation is certianly on an upward trajectory moving above target so the Bank of Canada is on track to taper its weekly QE asset purchases for a third time in July and rate hikes in the seond half of 2022. With all these factors in the melting pot, the scene is set for a robust economic recovery.

Inflation is coming back at a significant rate of knots at the same time as the economic recovery builds momentum. All eyes now turn to the ECB, but it is highly unlikely that they will be talking about tapering at the June meeting. In recent weeks we have heard from various ECB speakers talk against premature tightening and that inflation is expected to be temporary.

What is Driving Inflation? Energy inflation is the main culprit for the increase in prices. Oil prices have increased significantly over the last year and even with recent sideways movment since Febraury , Eurozone pertol prices hvae continued to rise modestly, reaching the highest level since mid-2019 two weeks ago. In conjunction with base effects, this has pushed energy inflation up from 10.4% in April to 13.1% in May. However, the base effect will moderate and this will reduce the impact of emergy inflation over the coming months, but don't think that this is the end to higher inflation. Inflation on goods will increase too and we are already seeing signs of this with higher input costs in manufacturing as well as supply chain issues, shortages and high capacity utilisation which are contributing to higher price pressuress. In May, it increased from 0.4% to 0.7%, and this is likely to continue trending up as supply chain issues continue for several months more and demand for goods remains strong. For services, it is a bit slower as COVID-19 restrictions are still in place in many countries. Reopenings are underway across the Eurozone but it is still a bit early to see the effect of these showing up in the numbers just yet and we may ned to wait until June to see this. Declining Unemployment Unemployment declined to 8% in April as the labour market continues to improve resulting from the lifting of COVID-19 restriction. However, the unemployment picture is affected by the furlough schemes that are still in place across the eurozone. This results in a very low unemployment rate and it will be intersting to see what happens when the furlough shcemes end. A strong economic recovery will ppotentially limit any layoffs that are delayed becuse of the furlough but we have to take into account that businesses have had to restructure through this pandemic and the lockdowns in order to survive. Cashflow and balance sheets have been damaged and there will be a lot of work to recover from this. Fortunately, there is pent up demand that will help in this recovery an potentially limit any impact on the labour market. We are already seeing strong demand which will boost GDP but also add to inflationary pressures. Higher Inflation - Temporary or Structural? With goods and services inflation set to increase more due to the reasons already mentioned, the question becomes, is this temporary or is this structural? ther eis no crystal ball for this and three will be extended debate on this for months to come. The economic recovery is building momentum but at some point after a few months of strong numbers, this will level off and we'll also see supply chain issues easing. As this happens, it is likely that in early 2022, we'll see inflation moderating. |

AuthorTim the trader Archives

January 2025

Categories |

RSS Feed

RSS Feed